The best funding option depends on two critical factors: your business’s profitability and how long you plan to remain actively involved.

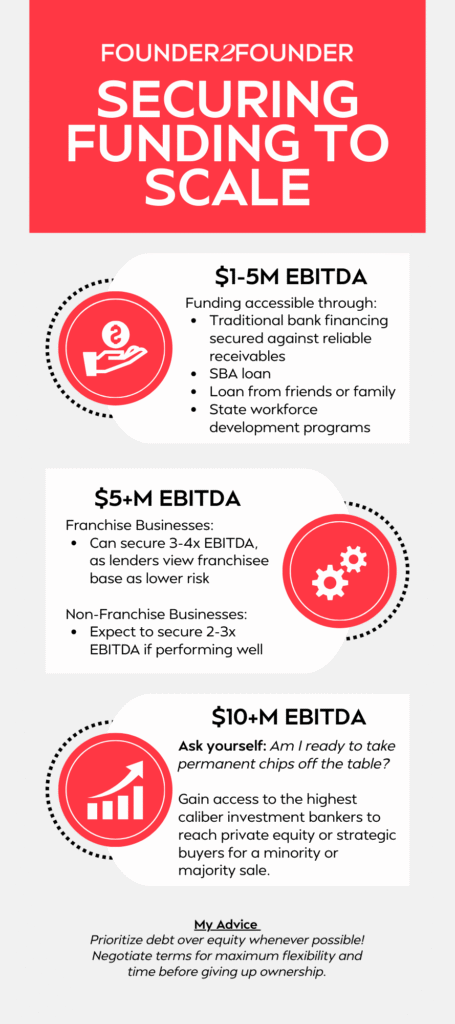

At $1-5M EBITDA

Traditional bank financing becomes accessible, typically secured against reliable receivables with 30-45 day payment cycles. This is often the cleanest option at this stage. Additional funding options include SBA loans, loans from friends or family, and state workforce development programs.

At $5M+ EBITDA

If you’re still passionate about the business and willing to delay personal distributions, you can access significant growth capital without personal guarantees. In franchising specifically, you can typically secure 3-4x EBITDA (roughly $15-20M at $5M EBITDA) because lenders view the diversified franchisee base as lower risk. For non-franchise businesses—whether in consumer goods or multi-site operations—expect a multiple of 2-3x EBITDA if the business is performing well.

My Advice: Prioritize debt over equity when possible. Negotiate terms without early payment penalties to buy yourself maximum flexibility and time before considering giving up ownership.

At $10M+ EBITDA

This is when you need to ask yourself: Are you ready to take permanent chips off the table? At this level, the best investment bankers are available to run a process to access private equity and/or strategic buyers. You can explore selling only a minority or selling the majority.

A critical warning about minority deals

Even if you only sell 40%, your partner will likely have control rights that make it feel like you sold the majority. Culture will shift. Your partnership becomes everything—choose extremely carefully. Sometimes taking more chips off the table through a majority sale is actually the better decision for your peace of mind and future.

Want to learn more about scaling? Watch The Best Levers for Scaling Your Business.

Community Q&A